In this episode I interview Jeffrey J. Pritchard, CFP®, CAP® about his new book, 529 Savings Plans for Grandparents Creating a Family Legacy of Higher Education.

For thirty-five years Jeff Pritchard has worked with some of the nation’s premiere wealth management organizations, advising families how to achieve their multigenerational financial and philanthropic goals. Jeff holds a Master of Business Administration degree (MBA), is a Certified Financial Planner (CFP) and a Chartered Advisor in Philanthropy (CAP).

He is the author of five other books and has been quoted in publications such as US News & World Report, Trusts & Estates, Money, USA Today, among others.

Below is the full transcript:

•••••••••••••••••••••••••••••••••••••••••••••••••••••••••••••••••••••••

Announcer: Welcome back America to Sound Retirement Radio, where we bring you concepts, ideas, and strategies designed to help you achieve clarity, confidence, and freedom as you prepare for and transition through retirement. And now here is your host, Jason Parker.

Jason: America, welcome back to another round of Sound Retirement Radio. So glad to have you tuning in this morning. We have a great episode lined up for you. This is number 192. I have a special guest that I’m going to introduce in just a minute. We’re going to be talking about 529 college savings plans for grandparents. But before we get into our topic, as you know, we like to start the morning two ways. The first is by renewing our mind. I thought this verse was really appropriate given this topic that we’re going to be talking about. This comes to us from Matthew 6:19. Do not store up for yourselves treasures on earth where moth and vermin destroy and where thieves break in and steal.

And then next one is, as you guys know, usually we have Amelia here to share a joke, but one of our listeners messaged me this one from LinkedIn. So the first circus man says I can’t be shot out of the cannon anymore. I’m retiring. And then the second circus man says what? You can’t retire. Where will I find a man of your caliber?

All right, episode 192. Today I have Jeffery J. Pritchard, CFP, CAP on the show with us. A little bit about him and then we’ll dig into it. But for 35 years, Jeff Pritchard has worked with some of the nation’s premier wealth management organizations, advising families on how to achieve their multi-generational financial and philanthropic goals. Jeff holds a masters of business administration, is a certified financial planner and a chartered advisor in philanthropy. He is the author of five other books and has been quoted in publications such as US News and World Report, Trusts and Estates, Money USA, among others. Jeff, welcome to Sound Retirement Radio.

Jeff: Jason, it’s great to join you.

Jason: Thanks. Hey, so the most important question I’m going to ask you this morning is, what’d you think of my joke this morning?

Jeff: Well, it’s kind of like the old circus joke of never following the animal acts. I would probably say don’t give up your day job. I got a chuckle out of it.

Jason: Well, I’m excited to have you on the program, especially because the topic of your new book, 529 College Savings Plans for Grandparents, and then the tagline is Creating a Family Legacy of Higher Education. So some of our listeners may not know what a 529 plan is. So I was hoping we could start with just the basics. What is a 529 plan?

Jeff: Well I think everybody knows how expensive college is and I won’t bore anybody with the details, but the federal government passed legislation to help families pay for college and a 529 plan, it’s very similar to a Roth IRA. It’s the saving and investment vehicle that allows families, parents or grandparents, to contribute into this plan and invest the money. And if the money is then distributed for what’s called qualified education expenses, you don’t pay tax on the gains. So it provides a vehicle for tax free, long-term compounding, which can, as you know, can really build up over time.

Jason: Yeah. Tax free. Those are the two words that many of the people that listen to this show really like the sound of, tax free use of money. So as we were talking before the show today, you shared with me one of the questions I said I had for you is do you have any grandkids? And you said, no I don’t, but you mentioned that you have already set up 529 plans for future grandkids. And that kind of boggled my mind. I hadn’t ever thought of that. Talk to us about why you would even do something like that.

Jeff: Well, first off that’s one of the things that I also found most compelling about these plans. The reason you can do that is the plans when you set them up, you assign a student or a beneficiary, but you can change who that student is as long as it’s a family member. So you can, in my case, I’ve set up a plan for both of my kids. Well they’re through school, but when they have kids I can transfer the beneficiary or the student into my grandchildren. But what that allows me to do it start building tax free growth long before those grandchildren are even born. So it’s a really a wonderful mechanism to start saving and growing that money.

Jason: Well that’s so cool. One of the things that, I just want to understand how you actually set the account up. You are the owner of the account and then you have the beneficiary listed as your adult child. Is that how it’s currently structured?

Jeff: You set up the account and you’re the owner of the account. That’s correct. And then you assign who that student is going to be. Now you can always change who that student is going to be down the road. So again, they’re very flexible plans.

Jason: So is that a key though when setting this up? You wouldn’t want to, if you have grandkids, you wouldn’t necessarily go set up a 529 and make the grandchild the owner of the account. Is that true?

Jeff: That’s true because the owner can pull the money out and if the owner is a minor, isn’t even the age of majority, it would have to be under a uniform gift to minors act, which gets very convoluted. So you’d set up the student or the grandchildren as the beneficiary. You, the grandparents or the parent, would always remain being the owner of that account.

Jason: And do people receive any kind of tax benefit when they put money into the, I know the answer to this, but for our listeners, do they receive any kind of tax benefit for putting money into the account?

Jeff: Well, if you live in a state that has a state income tax, now I live in Washington, which doesn’t have one, but most states do provide whether it’s a deduction on your state income taxes or our small matching credit, most of the states that have a state income tax provide a little extra incentive for money that these plans.

Jason: But no federal, not like an IRA where you get a deduction for funding it from a federal tax standpoint?

Jeff: No Jason. The money you put in is after tax. So again, it’s very similar to a Roth IRA where you’re putting after tax money into that plan, but it’s going to grow tax free for maybe several decades.

Jason: Once you’re gone, if you’re the owner, Jeff, you set this thing up and you name your child as the beneficiary and eventually you plan on changing it to your grandchild and then you die, let’s say you as the owner die, what happens at that point?

Jeff: It’s a cheerful question, Jason. Well, in the event that you are the owner of a plan, one of the questions that you’re asked when you set these plans up is who is your successor owner? Who is going to be the owner of this plan if you should pass away prior to the students going to college or whatnot. And so you name someone and it needs to be someone that you trust and someone who also wants those kids to have an education. Because one of the characteristics of these plans is the owner can pull the money back out and that’s very unusual. But the owner can pull the money back out.

So if someone set a plan up and they had an unexpected financial hardship, they could always get that money back. But it means if you’re appointing a successor owner in the event you die unexpectedly, you want to make sure that’s somebody that you really trust and that wants those kids or grandkids to also go to college.

Jason: Is there a penalty for pulling the money back out?

Jeff: There is, but it’s really not too bad. The penalty is that you would pay regular income tax on the gain. Plus there’s a 10% penalty on the gain. The key is that’s only on the gain.

Jason: Oh. That is [crosstalk 00:09:25].

Jeff: A lot of people confuse it with an IRA where if you pull money out of an IRA before you’re 59 and a half, you pay a 10% penalty on everything. But with a 529 plan, it’s only on the gain. So it’s a pretty inexpensive escape hatch if you need to pull that money out.

Jason: Boy that’s really good. You guys, if you’re just tuning in, you’re driving down the road in Seattle this morning, I Have Jeff Pritchard on the program with us. He just authored a new book called 529 College Savings Plans for Grandparents, Creating a Family Legacy of Higher Education. He set up a special website for the book. It’s called 529legacy.com. That’s the numbers 529legacy.com. And we’re talking about how you can leave an amazing legacy.

And you know, Jeff, I remember my dad said to me, he said you can make money, you can lose money. But he said once you have an education, they can never take that away from you. And that’s one of the reasons I thought that verse that I shared this morning was so powerful, do not store up for yourselves treasures on earth where moths and vermin destroy and where thieves break in and steal. Because when you gift something like a legacy, or as a legacy something like education, kids could squander money. They might go out and buy a sports car or a boat or something, just kind of blow it. But when you gift them education as a legacy, how cool is that? That’s something that once they have it, nobody can ever take it away from him.

Jeff: Yeah, that’s a very good point Jason. You can give somebody a vacation home. That can always burn down. You can give them [inaudible 00:11:01], they can be stolen. But you’re right, an education can never be taken away. And you consider all the potential doors it opens for young people, both from a career standpoint, from a social standpoint. But you’re spot on with what you say, Jason. Once somebody gets an education, that’s something that they’ll always have.

Jason: Yeah. I want to ask you about the flexibility because one of the things you talked about in your book is just how flexible these plans are and what they can be used for. We hope our listeners understand that.

Jeff: Yeah, so long as they’re used for what’s called qualified education expenses. And it’s not just, I think when we think of, we all think of college, but these are so flexible they can be used for tuition or not just colleges and universities, but also vocational or trade schools. Everything from [inaudible 00:12:01] school to a religious seminary school. So they covered tuition> they cover room and board. So the housing and the food costs so that the student while they’re pursuing higher education. They can be used for books, for computer equipment, for software, any required fees such as lab fees. So they’re really, really flexible.

And due to some recent legislation, they can now be used for K through 12 private school tuition. It’s a little controversial. But again, these plans are very, very flexible as far as what type of education expenses they can be used for.

Jason: Controversial, just in the sense that they’re intended for long term appreciation, capital growth, and then a distribution that in the future. What’s the controversy there?

Jeff: The controversy is with people like yourself, financial planners. They look at these and say well, the real advantage of these plans is, is this long term tax free growth. But if people start dipping into these sons prematurely to pay for a private grade school or something, you’re really defeating the purpose of having that longterm growth, you’re not able to do it. And then of course if they get into these funds to frequently for private grade school or middle school, is there going to be enough leftover for college, which is the real key. So that’s the reason they’re controversial, is doesn’t make financial sense to allow people to dip into these prematurely?

Jason: Yeah. Great. What about, I know in your book you talk about there are two types of 529 college savings plans. Will you help our listeners understand the two options that are available to them?

Jeff: Yeah, and again, the state I happen to live in, Washington, has both types. The first type is what’s called a prepaid college plan. And that’s essentially where you’re paying today’s tuition price, you’re paying that today for tomorrow’s tuition. So basically you contribute, you buy credits, semesters or quarters, whatever system your state might use. You’re paying today’s price and then the state guarantees that when your child or grandchild reaches the age of college, they’ll be able to use those credits for the same amount of semesters or quarters that you purchased at the current price. So the state than is required to invest those monies to make sure it keeps pace with tuition inflation.

The other type, which is more common and actually more financial planners recommended it, is a college savings plan. That’s what the book focuses on. And that’s somewhat similar to a, well maybe to an IRA where you’re putting money in and then you and your financial advisor is determining how to invest those funds. And 10, 20 years down the road, then whatever those funds have grown to, that’s what can be applied to the education expenses.

Jason: There’s been some controversy regarding the plan that’s available in Washington state and some people have made the argument that when it was first launched, it was a really, really great value. But now some folks are saying that boy, the breakeven based on the returns in those, it’s like four or five years I think is on the savings plan for Washington state. What is your opinion? If people have the option to choose between a prepaid college plan versus a savings plan, which one do you think makes more sense?

Jeff: Well, it does depend on the individual and what their priorities are. The problem with the prepaid plans, and right now there’s only 11 states that’ll let you, new students if you will, contribute into a prepaid plan. They’ve had some problems. And the problems are that they haven’t been able to keep pace with tuition inflation. And a lot of that is because legislatures around the country during the recession, they cut back budgets to state schools and the state schools had to increase the tuition price dramatically.

So basically a lot of states had to stop those prepaid plan and say, we’re not going to be able to afford this, and we’re not going to let any new people into these plants. We’ll honor the past students, but we’re not going to let any new people into this. And that’s kind of a problem. So most financial planners I’ve spoken with on this, they tend to lean towards the savings plans. Now Washington state is one of the better funded prepaid plans and it has one of the better guarantees. So it’s one of the better prepaid plans.

But kind of generically, most advisors recommended the college savings plan approach.

Jason: And then once they have the 529 established in the savings plan option, what are the investment options? How can the money be invested in those accounts?

Jeff: Well, and it’s a good question Jason because that’s obviously a key element. There’s three options. The first is basically build your own portfolio. The states provide a very broad menu of mutual funds and ETFs and index funds and whatnot. And as the name implies, you and your financial advisor use that menu funds to build your portfolio.

The second method is what’s called a static portfolio. That name’s a little confusing, but basically you choose among pre allocated portfolios. They have a mixture of all those various funds and you’re normally just selecting whether you want an aggressive portfolio or a conservative portfolio or a middle of the road. But those portfolios stay in that aggressive or conservative mode as long as you have them.

The third option, and what is probably the best, particularly for people who are kind of going to go alone on this and not use an advisor, it’s called an age based portfolio. And as the name implies, this is based on the age of the student, or the beneficiary of the plan. How old is the student? If you set this up when the student or the grandchild or the child is only two years old, that portfolio will start out being fairly aggressive. But as the student ages year after year and they get closer and closer to college, when they’re actually going to need that money, the portfolio is automatically made more and more conservative so it has less risk and less volatility. The idea being you’re not subjecting that student to a bear market and they lose half their money just at the point when they need to use it for college.

So those are the three types. And again, I think if someone’s working without a financial advisor, the age based portfolio is normally recommended. But if you’re familiar with investments and you enjoy that then you can always build your own.

Jason: If somebody has, say somebody has five grandchildren, because these accounts are so flexible and that you can change the beneficiary at any time, should people set up five individual accounts, five different 529s for each grandchild? Or should they just have one 529 and change the beneficiary depending on who’s in college at that time?

Jeff: They could probably do either. I mean you could do either. Probably just from a simplicity standpoint, having a different one for each grandchild, it’s appropriate, particularly since those grandchildren are going to all be different ages. And so if you’ve got a grandchild that 12 and one that’s three, they probably out to be in very different portfolios. So if it’s all in just one bucket, you kind of get that all mixed up. Whereas if you have an individual plan for each grandchild or child, that portfolio, those investments can be customized for how old the grandchild is.

Jason: That’s how I did it with our kids, is I have one 529 plan for each one of them. And we keep them separated. I wanted to ask [crosstalk 00:21:00]. I wanted to ask, if parents and grandparents or students themselves have a 529 plan, does that disqualify the student from financial aid consideration?

Jeff: It doesn’t. Now, if the plan is huge, like a million dollars or something yes but it doesn’t. It’s fairly complicated administratively. If the parent owns a plan, it reduces financial aid qualification a little bit. Actually if a grandparent owns a 529 plan, it has no impact on financial aid consideration from the grandchild until distributions are made. It actually is somewhat complicated, can require a little administrative nimbleness. And I go into quite a bit of detail in the book on how to work around that. But the short answer is having a 529 plan does not disqualify that student from financial aid.

Jason: One of the things that I had heard one time, Jeff, and tell me if this is still the case, but for grandparents that have these 529 plans, one of the things that they’ll do is they’ll wait till college is completely finished before they make a distribution from the 529 plan. Is that still a good strategy just in terms of keeping the account in waiting to use it until the child finishes or the grandchild finishes college to make the distribution?

Jeff: Well, two things. First is, if the expenses for college don’t match the distributions from a calendar year standpoint, the IRS may not like that. Otherwise you could wait 20 years until you distribute. If you’re talking about financial aid, the ideal is for a grandparent to wait until the student is a junior because the financial aid, the FAFSA form gives kind of a two year window or break so that those distributions don’t count against financial aid consideration for a two year look back.

So it’s a little confusing but I don’t think you’d want to wait till the student was completely done with school. It could create some red flags with the IRS.

Jason: Okay, very good.

Folks, you’ve been listening to episode 192 on Sound Retirement Radio. Find us online at soundretirementplanning.com. I’ve been interviewing Jeff Pritchard, Jeffrey Pritchard regarding new book 529 College Savings Plans for Grandparents, Creating a Family Legacy of Higher Education. Jeff, set up a website at 529legacy.com where you can learn more and buy the book there or buy it on Amazon. Jeff, thank you so much for being a guest on Sound Retirement Radio today.

Jeff: Jason, I enjoyed it thoroughly.

Jason: Thank you.

Announcer:Information and opinions expressed here are believed to be accurate and complete, for general information only and should not be construed as specific tax, legal, or financial advice for any individual. And does not constitute a solicitation for any securities or insurance products. Please consult with your financial professional before taking action on anything discussed in this program. Parker Financial, its representatives or its affiliates have no liability for investment decisions or other actions taken or made by you based on the information provided in this program. All insurance related discussions are subject to the claims paying ability of the company. Investing involves risk.

Jason Parker is the president of Parker Financial, an independent fee based wealth management firm located at 9057 Washington Avenue Northwest, Silverdale, Washington. For additional information, call 1-800-514-5046 or visit us online at soundretirementplanning.com.

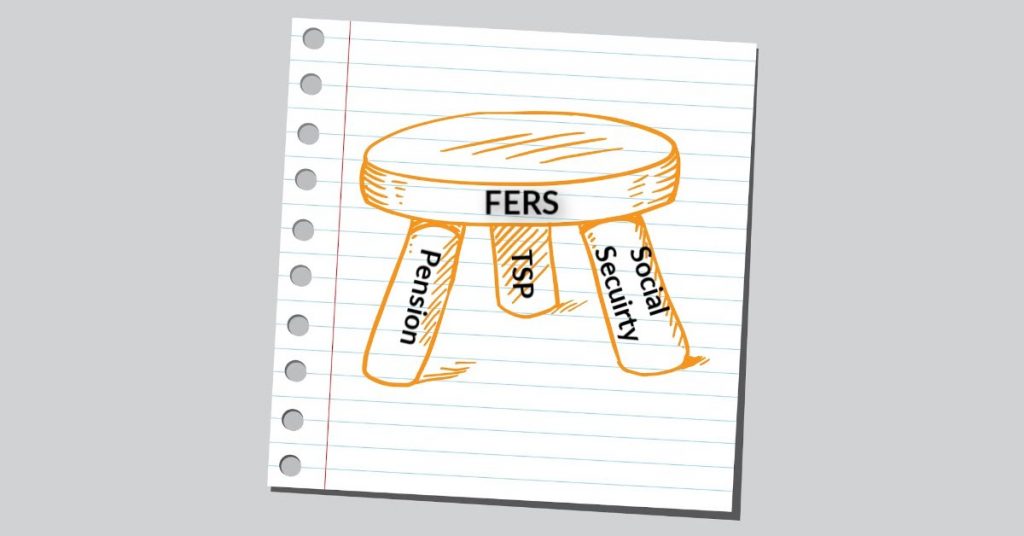

The Ultimate FERS Retirement Resource Page

FERS Pension, TSP, Social Security

Available on Amazon