If you had money available to earn interest, then which would you rather have?

- $84 of interest in one year?

- Or $797 of interest in one year?

That is a 948% difference in the amount of interest after just one year, and I’m going to share with you exactly how and why you might want to consider an alternate vehicle for your money.

I recently had a client contact me and she said, “Jason I have a CD at the credit union that is about to mature.” She went on to say, “Last year I earned about $75 of interest on $29,000. The CD is going to rollover soon, and the new rate is only going to be 0.29%.”

Yes … you read that correctly.

She will earn a little more than ¼ of one percent if she leaves her money at the credit union. I’ve found some people mistakenly move the decimal point and think they are earning 2.9%. Not in this case. She would in fact be earning only 0.29% percent for a one year certificate of deposit. This is why some people now say “CD” stands for certificate of disappointment.

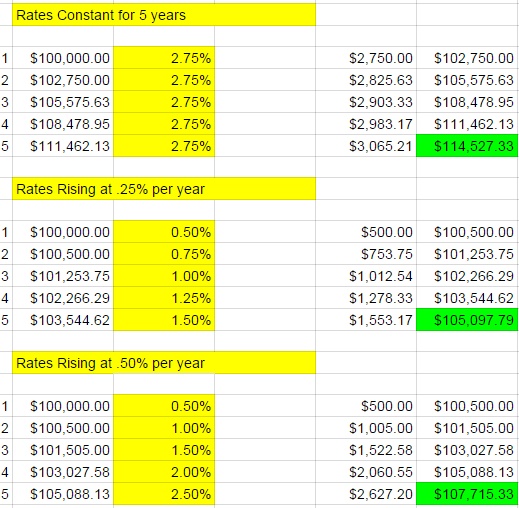

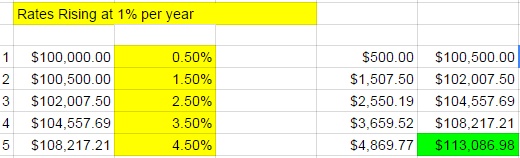

When it comes to safe money, in order to get a higher fixed interest rate, you generally have to commit to a longer period of time. For this client we were able to find a fixed deferred insurance contract that guaranteed 2.75% interest if she would commit to a five year term. In the historic context of interest rates, 2.75% does not sound very good. But if she earns 2.75% interest on $29,000 the first year, then she will earn $797 of interest. If she sticks with the CD she would earn about $84 in interest. Given the options she has available today, I’d say the choice is pretty straight forward.

But what if you commit to five years and then interest rates go up?

Many people don’t like the idea of committing to a five year period of time in a low interest rate environment, but there may be a cost to keeping short term CDs. I created a quick spreadsheet to try and determine the cost of keeping the CD’s short term assuming the CD is rolled over every year and every year interest rates are going up.

You can see the results below. I assumed a couple of different scenarios with interest rates rising: .25%, .50%, .75% and 1% every year for the next 5 years. I’ve highlighted in yellow what the value of her account will be at the end of five years given the different scenarios.

Obviously there is a cost of waiting.

This article was also featured in the January Kitsap Peninsula Business Journal.